Which Best Describes a Credit Default Swap

It exchanges the realized return on an asset including both income and capital gainslosses for a return equal to LIBOR plus a spread on the initial value of the asset. Which of the following best describes a credit default swap.

Credit Risk Transfer Mechanisms Frm Analystprep

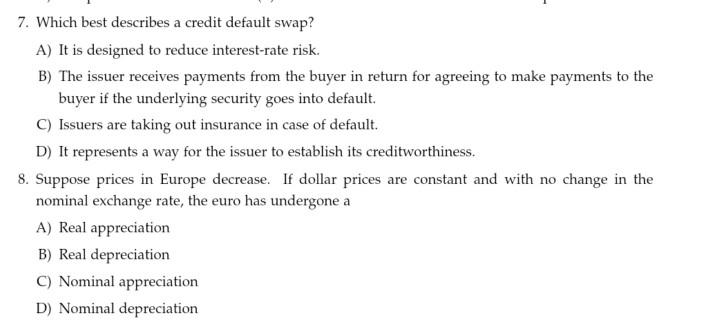

A It is designed to reduce interest-rate risk.

. My words-not grade A key reason that firms and financial institutions might participate in an interest rate swap isto transfer interest rate risk to parties that are more willing to bear it. Which of the following best describes a total return swap. It is protected against default b.

Which of the following best describes Galts debt using a call option. Asked Aug 17 2017 in Business by SingleMind. Investments 9th Edition Edit edition Solutions for Chapter 14 Problem 27P.

A It is designed to reduce interest-rate risk. Which of the following most accurately describes the behavior of credit default swapsa. The CDS purchaser pay annual premium to the seller of the swap and in return collect the payment in case of default and it work as an insurance against the non-payment of the fixed liability.

It can be thought of as insurance against credit risk. When credit and interest rate risk increase swap premiums increasec. ALong 700 million in the firms assets and Short a call option with a 700 strike price B.

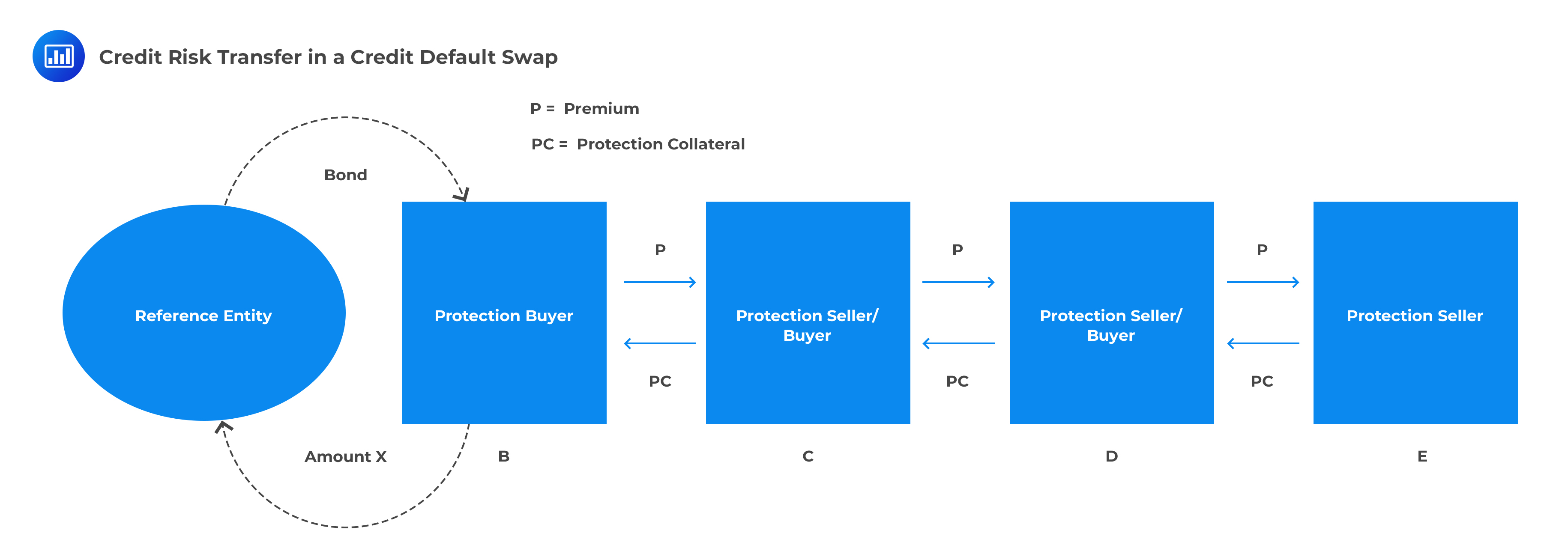

Single-credit CDS referencing specific corporates bank credits and sovereigns. C Issuers are taking out insurance in case of default. A credit default swap CDS is a particular type of swap designed to transfer the credit exposure of fixed income products between two or.

When credit risk increases swap premiums increase but when interest. C The issuer receives payments from the buyer in return for agreeing to make payments to the buyer if the security goes into default. Which best describes a credit default swap.

That is the seller of the CDS insures the buyer against some reference asset defaulting. Credit default swap is used to transfer the credit risk exposure which arises from the fixed income securities such as bond. Unfortunately LMN goes bankrupt a year after this swap agreement becomes.

All of the following describe the market for credit default swaps. The ABC Bank enters into a credit default swap with XYZ Financial. It off if another party external to.

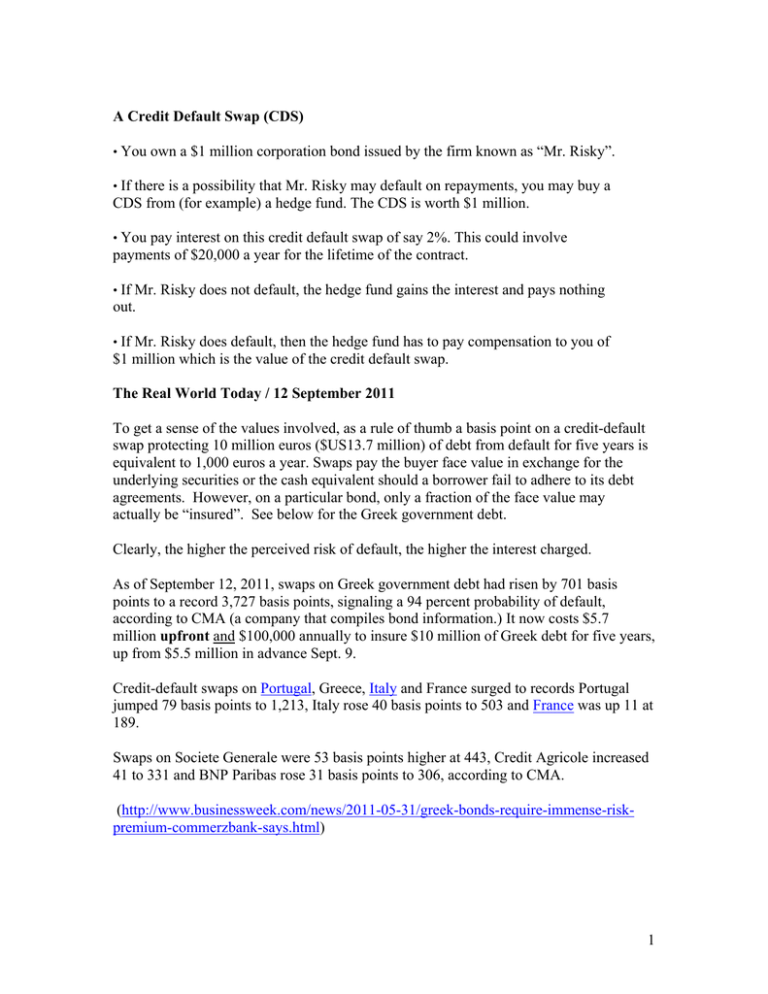

The credit default swap market is generally divided into three sectors. When credit risk increases swap premiums increaseb. C Issuers are taking out insurance in case of default.

Credit default swap Crisk-free swap Dinterest rate swap. The swap runs for 5 years and is based upon a term loan to LMN Corp. The size of the protection payment is 5 per year.

The issuer receives payments from the buyer in return for agreeing to make payments to the buyer if the security goes into default. C Issuers are taking out insurance in case of default is the best answer. D It represents a way for the issuer to establish its.

117 All of the following describe the market for credit default swaps on mortgage-backed securities in the mid-2000s EXCEPT A an increasing number of buyers were speculators. A limitation of interest rate swaps is that there is a risk to each swap participant that the counterparty could default on its payments. Which best describes a credit default swap.

Which of the following best describes a credit default swap. B The issuer receives payments from the buyer in return for agreeing to make payments to the buyer if the underlying security goes into default. Which best describes a credit default swap.

166 Credit derivatives BLM. Which best describes a credit default swap. Agreement to pay if party defaults on loan payments.

D It represents a way for the issuer to establish its creditworthiness. When credit risk increases swap premiums increase but when interest rate risk increases swap premiums decrease. D Issuers are taking out insurance in case of default.

Seller of the Swap. -a product that acts like a pre-bundled portfolio of single-name credit default swaps-a proposed product that would make payments based on credit spreads rather than events-a new product that publishes market prices in the same manner as traditional equity indices-a defunct product that made payments based on the market value of a cash bond index. The credits referenced in a CDS are known as reference entities.

When credit and interest rate risk increases swap premiums increasec. B The issuer receives payments from the buyer in return for agreeing to make payments to the buyer if the underlying security goes into default. Asked Aug 17 2017 in Business by VonDutch.

Multi-credit CDS which can reference a custom portfolio of credits agreed upon by the buyer and seller CDS index. Credit Default Swaps CDS are a bilateral OTC contracts that transfer a credit exposure on a specific reference entity across market participants. These contracts are linked to either a.

It exchanges the promised return on an asset including both income and capital gains. Business Finance QA Library Which of the following most accurately describes the behavior of credit default swapsa. It has a higher rate to compensate for the possibility of one party defaulting c.

In very general terms the buyer of a CDS makes periodic payments in exchange for a positive payoff when a credit event is deemed to have occurred1. The Correct answer is B Option ie. Buying protection has a similar credit risk position to.

When credit risk increases swap premiums increaseb. A It is designed to reduce interest-rate risk. A Credit default swap is a financial swap agreement that the seller of the Credit default swap will compensate the buyer in the event of a default.

Credit Default Swaps CDS A credit default swap is an agreement between the buyer and seller to exchange the borrowers credit risk. It carries a higher credit rating than most other swaps d. The CDS buyer buys protection by making periodic payments to the seller until the end of the CDS life or a credit event occurs.

A credit default swap is when the issuer of a bond ends up. C Issuers are taking out insurance in case of default. B The issuer receives payments from the buyer in return for agreeing to make payments to the buyer if the security goes into default.

Share this link with a friend.

/78293570-5bfc2b8cc9e77c0026b4f8e9.jpg)

Credit Default Swap Cds Definition

A Credit Default Swap Cds

Solved 7 Which Best Describes A Credit Default Swap A It Chegg Com

No comments for "Which Best Describes a Credit Default Swap"

Post a Comment